Maintaining living standards in retirement

- On 11/06/2019

- retirement

On Wednesday, 5 June 2019, ASIC announced[1] that it had amended the relief conditions for superannuation and retirement calculators. Specifically, ASIC has removed the requirement that superannuation and retirement calculators discount at a fixed rate of CPI – 2.5% – and instead encourages providers of these tools to use a higher rate that allows for rising community living standards beyond keeping up with inflation.

Though it sounds uninteresting, the difference can actually be significant. The policy change from ASIC is a big win (following more than two years of consultation) for the industry and providers of these calculators everywhere. Rice Warner provides online tools and calculators to many funds, insurers and financial planners. Our tools are all powered by PHOEBE calculation engines. This engine was also used for the recent policy paper released last week[2].

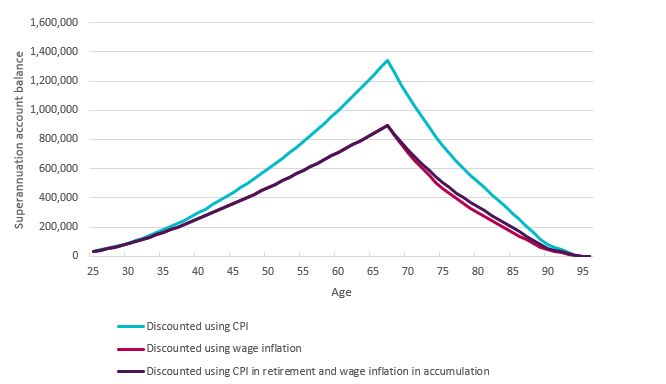

The key takeaway is that ASIC has confirmed the importance of maintaining living standards (not purchasing power) in retirement – policymakers take note. Graph 1 demonstrates why this is important, because it may overstate retirement balances by as much as 50% relative to using a wage deflator.

Users of online tools and calculators are unlikely to appreciate the impact of this relatively obscure assumption so its important that the defaults are set appropriately. But to put it simply, it would mean the difference between you retiring with a Nokia, which you may have used 15 years ago, versus an iPhone – or the future equivalent depending on your age!

Graph 1. Impact of discounting on superannuation fund balances – CPI (2.5%), wages (3.5%) or mixed (CPI – retirement, wages – accumulation)

Price-based discounting may be disadvantageous for full career projections as the Age Pension is indexed to wages and will grow in real terms over the entire period. Under such a scenario, researchers will find that the Age Pension will sufficiently cover most of the adequate benchmark.

There is also near universal support for maintaining indexation of the Age Pension to wages, given that it would quickly reduce below community expectations were it to be indexed to prices.

Despite this, there is a growing body of research suggesting that, given that the actual expenditure of retirees is likely to fall during retirement, wage-based indexation sets too high a standard. This argument is reasonable (given expectations on expenditure across the three phases of retirement) though the evidence based on available data is mixed as few good longitudinal datasets are available and much of the analysis relies on cross-sectional studies or limited longitudinal studies that rely on small samples over short periods of time.

Overall, the impact of price-based discounting in retirement only is smaller as the time horizon is shorter. It is a reasonable assumption for public policy work though our preference is to use wages throughout for online tools and calculators to avoid confusing consumers and to show the Age Pension as flat in real terms.

The ongoing debate about discounting during the retirement phase shows that more work needs to be done before industry and policy makers can agree on the right assumption.

This work should focus on understanding the spending needs of retirees in different cohorts (or generations), sensitivities around these assumptions (for example, differing needs of renters and homeowners, singles and couples) and how these spending needs change throughout retirement including the transition to aged care.

[1] https://asic.gov.au/about-asic/news-centre/find-a-media-release/2019-releases/19-129mr-asic-amends-relief-conditions-for-superannuation-and-retirement-calculators/

[2] https://www.ricewarner.com/what-is-the-right-level-of-sg/