How consolidation will shape the industry

- On 23/02/2017

- superannuation

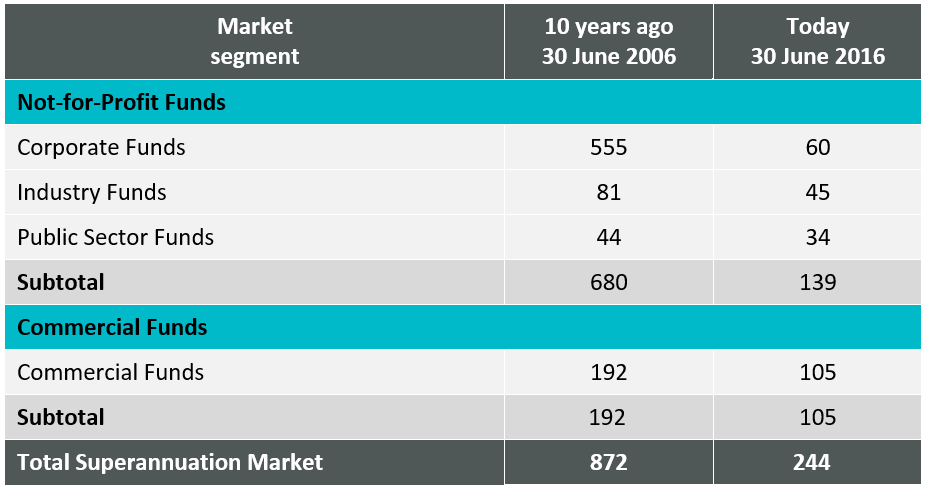

Each year Rice Warner’s Superannuation Market Projections Report comments on the level of consolidation that has occurred in the industry. The decade leading to 2016 has seen the industry, not including SMSFs, shrink from 872 funds to 244 – a fall of 72% in just 10 short years.

Table 1: Number of funds

There are a number of significant and well documented forces shaping the superannuation industry– demographic shifts, rising member balances, technological changes and legislative evolution – but consolidation within the industry has and will continue to be one of the main driving forces that shapes the industry.

There are a number of significant and well documented forces shaping the superannuation industry– demographic shifts, rising member balances, technological changes and legislative evolution – but consolidation within the industry has and will continue to be one of the main driving forces that shapes the industry.

Regulatory and competitive pressures are mounting

In April 2015, APRA issued shots across the bows of underperforming funds when Helen Rowell suggested that the regulator was expecting continued consolidation and would focus on ensuring that trustees were proactive about their future, including the possibility of mergers ¹. When funds created their MySuper products, they provided a three-year business plan. None anticipated negative growth in membership.

Yet many funds are shrinking. In 2016 there were 83 of 219 funds with negative net flows. It is not reasonable to expect these funds to be able to provide their members with the best possible service whilst under this type of fiscal pressure.

Additionally, funds compete now on services more than at any other point in the history of superannuation. Industry and Retail funds alike have both utilised scale to offer better rounded products and services to their members, in part to try to slow the outflow of retirement funds to SMSFs. Smaller funds will find themselves unable to compete effectively as this continues, and the upcoming framework for retirement products (CIPRs) will likely exacerbate the divide.

Rice Warner research into superannuation fund expense levels has confirmed that scale benefits are a major driver in reducing costs. Operating expenses reduce significantly with scale. In particular, funds with more than $10bn tend to have materially lower investment expenses than other funds.

This information suggests that continued rationalisation will benefit both members and the industry as a whole. Additionally, we consider that there exists scope in the short term for additional activity based on the current composition of the industry.

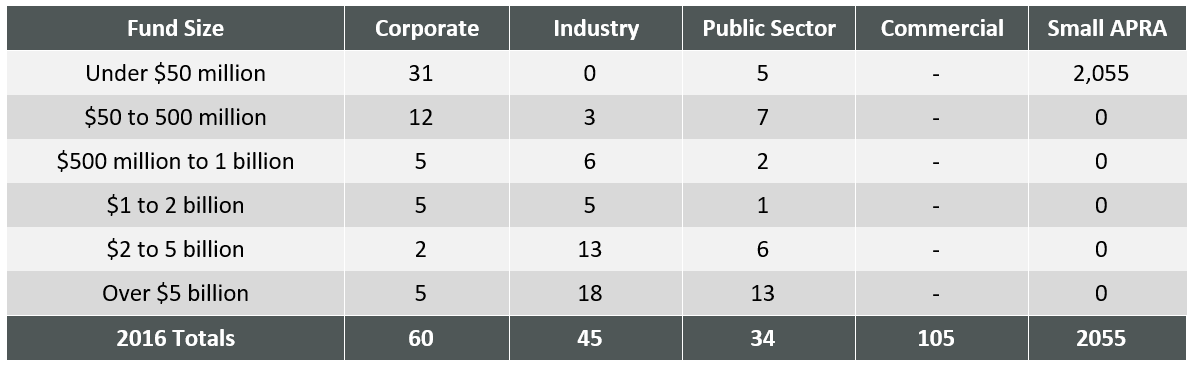

Table 2: Fund size

It is worth pointing out that simply having scale will not be enough unless it is being used effectively. A large provider with legacy systems and products will have no advantage compared to a medium sized organisation that makes effective use of large suppliers and partnerships with other organisations.

It is worth pointing out that simply having scale will not be enough unless it is being used effectively. A large provider with legacy systems and products will have no advantage compared to a medium sized organisation that makes effective use of large suppliers and partnerships with other organisations.

What will the future look like?

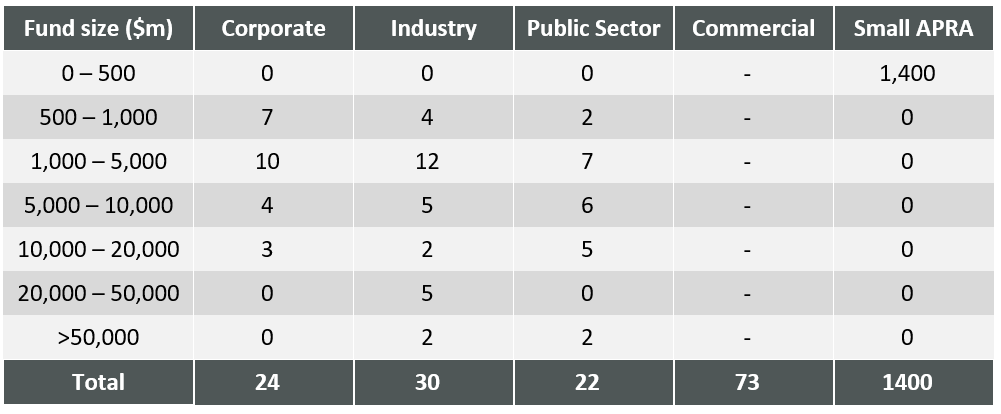

Rice Warner believes that the coming 5 years will include significant merger activity. Our estimated future profile of the industry is given below.

Table 3: Estimate of number of funds June 2021

We observe significant momentum for consolidation activity. Funds are attracted to the idea that through scale they can provide additional member services without increasing charges for members.

We observe significant momentum for consolidation activity. Funds are attracted to the idea that through scale they can provide additional member services without increasing charges for members.

¹ http://www.apra.gov.au/Speeches/Pages/The-super-system—what-is-on-APRA’s-watch-list.aspx