Superannuation objectives

- On 13/04/2016

Objective(s) of superannuation

Rice Warner is broadly supportive of the Financial System Inquiry’s (FSI) recommended primary and subsidiary objectives of superannuation but with some reservations and suggestions.

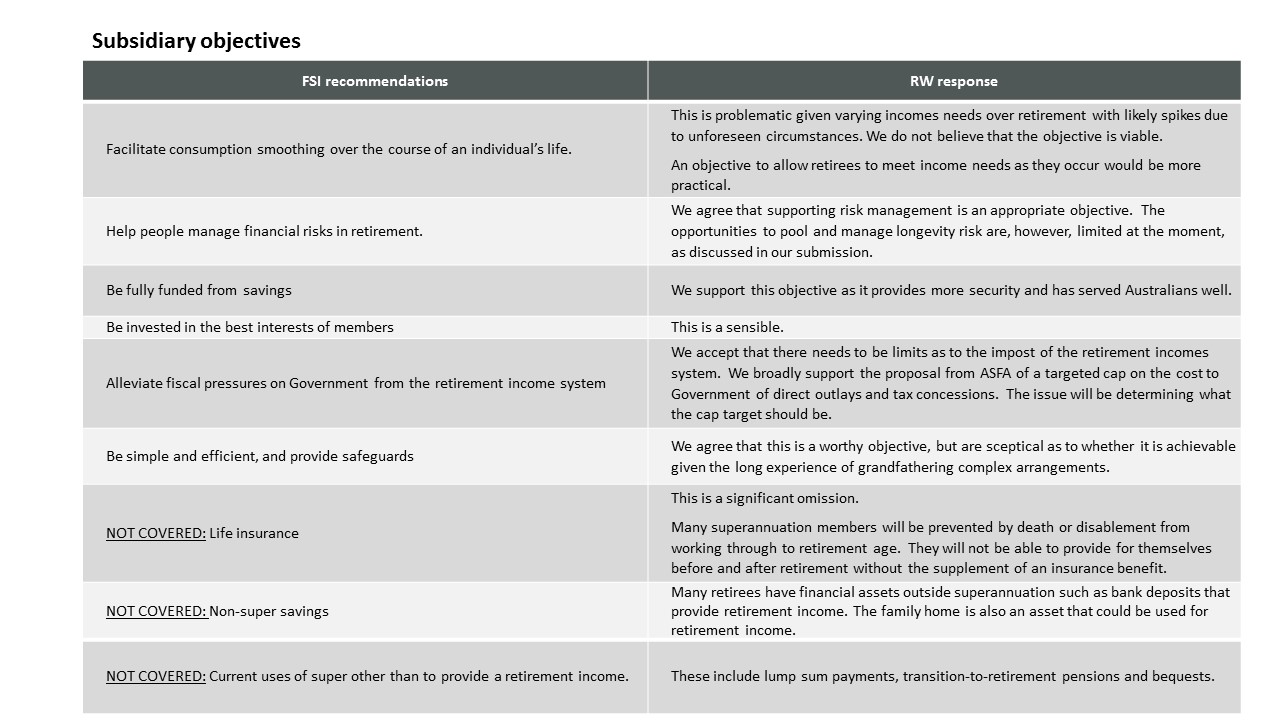

We suggest that the primary objective is extended to cover “adequacy” of retirement income and point to the significant omissions in the subsidiary objectives of the roles of life insurance and non-superannuation savings.

Our comments are in Rice Warner’s submission in response to the recent Treasury discussion paper Objective of Superannuation.

We support the approach of having an overarching, primary objective for superannuation. All future changes should be measured against this objective – before being introduced. Yet a single, simple statement is unlikely to provide sufficient focus and would probably become just a slogan.

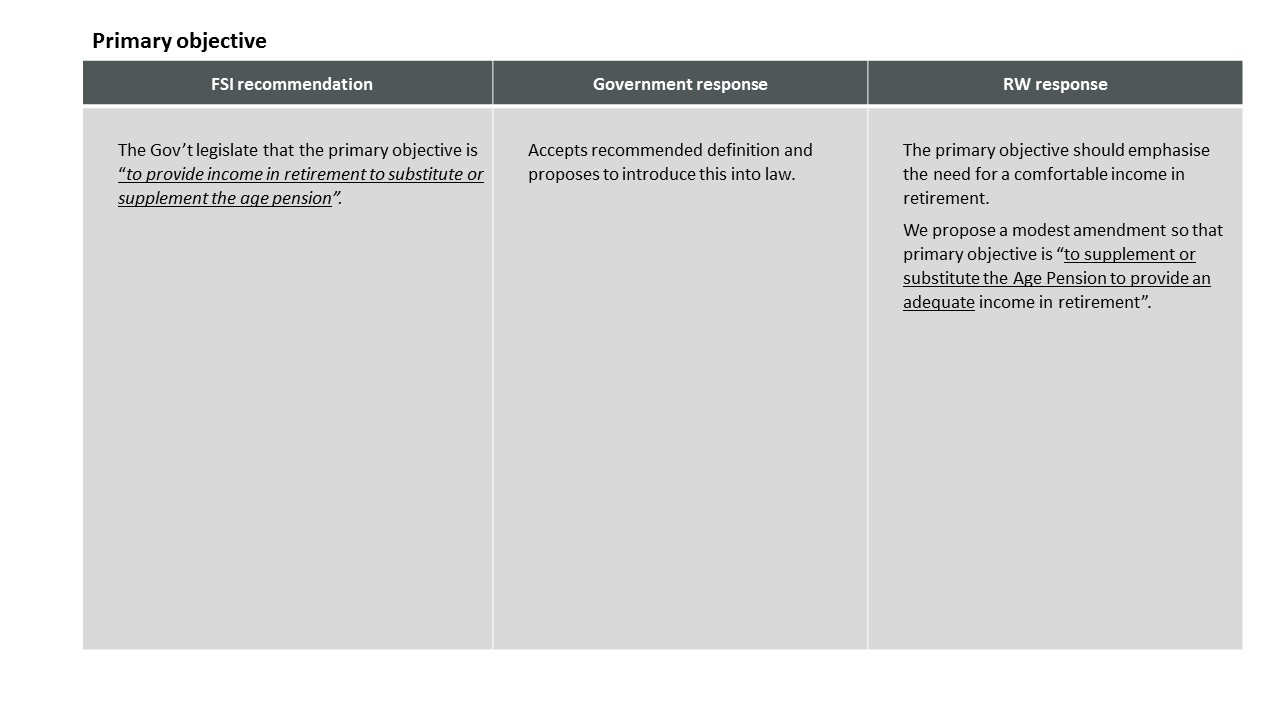

Primary objective

Rice Warner proposes a small amendment to the FSI’s recommendation so that the primary objective is

The adequacy of retirement incomes is a critical component of Australia’s retirement incomes system. The Age Pension should be set at a level sufficient to keep all pensioners out of poverty. In turn, superannuation should aim to provide as many Australians as possible with a comfortable living in retirement.

Cost and sustainability

As discussed in our submission, Australia’s superannuation system is structured in a way that will provide an adequate retirement income for those who are prepared and able to sacrifice sufficient current income. However, if the system allows people to generate benefits that are far in excess of adequacy, then tax concessions are poorly targeted.

Fiscal sustainability will require an equitable balance between direct Government outlays and tax concessions. If more is to be done alleviating poverty in retirement, concessions need to be better targeted to free up funds.

Other uses

Superannuation is currently used for a range of purposes not specifically covered by the primary objective of providing a retirement income. Consideration should be given as whether or not such other uses of superannuation should be limited in any way – and this should be reflected in the subsidiary objectives.

Such uses include the payment of typically small lump sums at retirement and in retirement, transition-to-retirement pensions while working and bequests.

Most retirees appear frugal in their spending yet need lump sums on occasions to pay for emergencies. And although transition-to-retirement pensions are not technically used for retirement income, many workers use these to boost inadequate retirement savings.

1 Comment