Super ambitions: Can we get to $1.6 million-plus?

- On 20/07/2016

There is much misinformed comment that two of the Federal Budget’s core superannuation proposals will significantly hamper the ability to save in superannuation. It has been stated that fund members who can afford to make large contributions will not be able to reach the new pension cap of $1.6 million. However, modelling by Rice Warner gives a different impression.

The two proposals are, of course, the $500,000 indexed lifetime cap on non-concessional contributions (including past contributions from July 2007) and the cutting of the annual cap on concessional contributions to a flat $25,000.

What our modelling shows

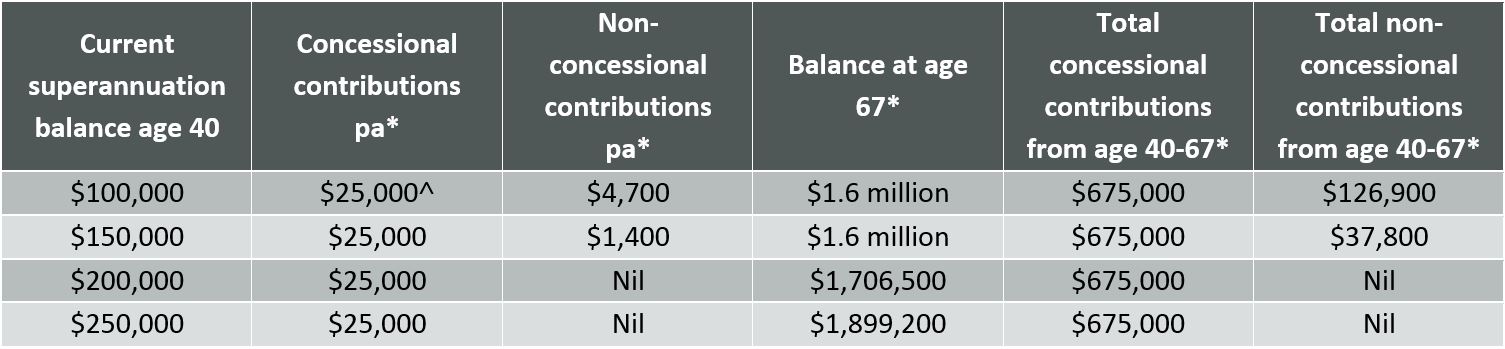

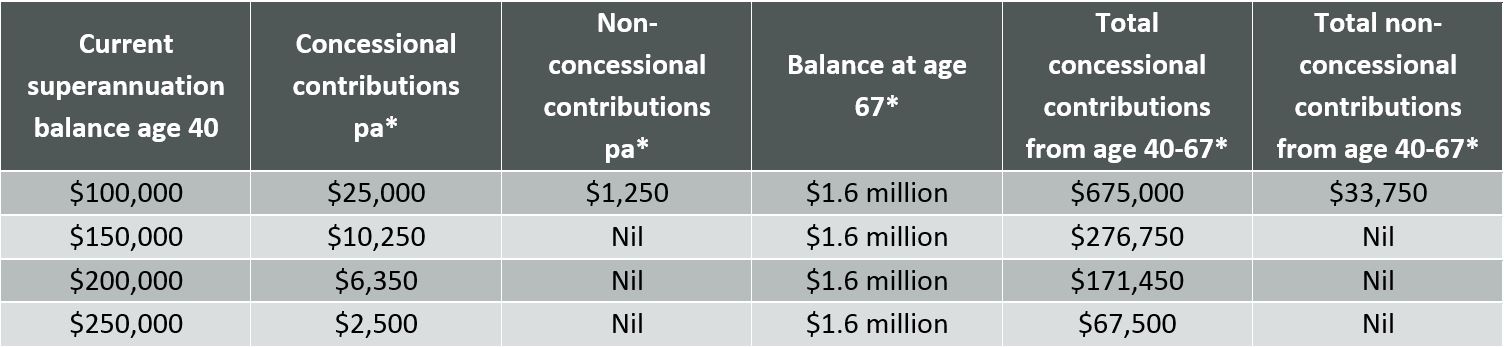

As set out in the tables, Rice Warner has prepared eight case studies of fund members aged 40 with an intention to retire at 67 (the future eligibility age for the Age Pension). Four of the members are currently earning $100,000 a year with the other four earning $250,000 a year. Their existing superannuation balances range from $100,000 to $250,000.

The modelling shows that each of the fund members can save at least $1.6 million in superannuation, the Government’s proposed cap on amounts transferrable to a pension account.

Based on certain assumptions including an annual (long-term) fund earning rate of 6.5% and wage inflation of 4%, we calculate that:

- Five of the eight fund members in the case studies will reach at least $1.6 million without having to make any more non-concessional contributions. Significantly, the remaining three will need to make only modest annual non-concessional contributions.

- Each fund member will mainly rely on the combination of concessional contributions (in some cases markedly below the proposed annual cap on these contributions) and the investment earnings of their funds, utilising the benefits of compounding returns over 27 years.

We also note that members who are able to accumulate more than $1.6m can keep the excess funds in a concessionally taxed accumulation fund.

Tweaks to reduce the heat

Certainly, there are other circumstances when a $500,000 non-concessional lifetime cap would not be enough to make $1.6 million in superannuation by retirement. Such circumstances may include members, perhaps in their fifties, who have little superannuation savings to date and want to ‘catch up’.

Another case the Government could consider would be to have some leniency for fund members who have re-contributed their transition-to-retirement pensions back into superannuation as non-concessional contributions.

Perhaps some re-contributed amounts could be excluded from the lifetime cap.

Finally, criticism caused by counting non-concessional contributions back to July 2007 in the lifetime cap could be reduced or removed. One way would be to limit the amount that the cap could applied to past contributions to, say, $250,000.

It is clear that the Government will aim to remove much of the angst triggered by its proposals while still achieving its broad objectives, which include making the superannuation system more equitable.

High-income earner: $250,000 today

Middle-income earner: $100,000 today

˄ proposed concessional cap

*today’s dollars.

Assumptions: Fund earning rate 6.5%, account fees 1%, CPI 2.5%, wage inflation 4%.

Note:

- Government’s proposed $500,000 non-concessional cap and $1.6 million cap on pension accounts are indexed. Under Budget proposals, concessional contributions of higher-income earners will become liable for Division 293 tax.

- Concessional contributions are subject to tax at 15%, those earning over $250,000 in Adjusted Taxable Income will pay tax at a higher rate of 30%. Subsequently, for these members a contribution of $25,000 will only be $17,500 after tax.

This Insight has been updated. To view the latest version, click here.

5 Comments