Retirement Planning in a disjointed system

- On 23/05/2019

- retirement

During the Federal election, the Coalition promised not to make any changes to superannuation in the term of the new Parliament. Despite this promise and its re-election, this does not mean we will have a period of stability – the industry still must deal with the Protecting Your Super Package and the enhanced requirements of APRA’s new Member Outcomes regime. Further, the government will consider and for the most part implement the recommendations of the Royal Commission into Misconduct in the Banking, Superannuation and Financial Services Industry.

While the industry would welcome a break from constant change, it is likely that we will see more reforms. One of the areas needing immediate attention is support for people approaching retirement. Engagement and financial advice for these members is variable and sporadic; many funds would struggle to pass a sound Member Outcomes test in this area.

WHAT HAPPENS NEXT?

The path to retirement is clouded by the need for information and financial advice as members will be confronted with some complex issues. There are several key decisions to be made.

Approaching retirement

Most superannuation funds have calculators projecting benefits at retirement and a few show the expected income in retirement. However, the funds do not know much about a member’s personal financial circumstances, so these calculations can only be a crude guideline. Some funds have set up good calculators where the member can actively engage by entering their personal information. However, they will still need someone to explain the output.

Members will start thinking about retirement a few years beforehand, and this is where the fund can really add value. More than two-thirds of members will be married, so they also need to consider their combined financial situation and likely timing of their partner retiring. They should be told of the need to protect themselves against sequencing, longevity and investment risks – but are unlikely to be equipped to deal with these issues. Even a simple decision such as how much monthly benefit to draw is difficult as they cannot be sure how long their money will last. This will depend on unknown factors including how long they live, how much they need to budget and what investment earnings they will receive in retirement. For many, the Age Pension will be the greater part of their retirement income and the rules around that are complex too, with an income and an assets test, and a history of Government changes in means testing rules.

Members may want a lump sum at retirement to pay off debt or perhaps for home renovations or a holiday reward. Some members will continue working part-time to supplement their pension benefit, but they may be confused by the complexity around eligibility for the Age Pension, which affects most retirees.

Clearly, members require guidance and it makes sense for their superannuation fund to provide this, particularly if they are delivering the required pension product. However, the existing system is flawed with two major problems, which remain unaddressed despite the plethora of superannuation inquiries imposed on the industry:

- The financial advice laws (reinforced by commentary from the Royal Commissioner) assume a financial adviser is independent only if they are not commercially linked to a product provider. However, members need strategic advice even if they are content to use the building blocks of their current fund (or product provider).

- There is no default product for retirement. All members entering retirement must sign up for a new (Choice) product.

In retirement

In retirement, member needs will be linked to their personal circumstances. For budgeting, most will supplement the Age Pension with their superannuation pension. They may put money into a cash account to finance pension payments over the next one to three years. The rest of the benefit might be placed into a growth account recognising the need for inflation and longevity protection.

The decisions then come down to:

- Do we want more certainty about the future, even if this means sacrificing potential returns?

- Do we need a nest egg for emergencies (including Aged Care late in life)?

- Do we want to leave a bequest for the children?

- Do we need to adjust the pension payment? (Many retirees spend less as they age).

The overarching theme of most financial advice will be around reviewing their budget. For example, the fund had a great performance last year, so can we take some of the profit and use it on a holiday?

The nature of this advice is that much of it could be delivered by algorithms. These could also be used to top up the cash account periodically to provide liquidity for pension payments and lock in outperformance against objectives. Clearly defined default algorithms can help members who prefer to rely on a professionally managed default product.

PUBLIC POLICY DEVELOPMENTS

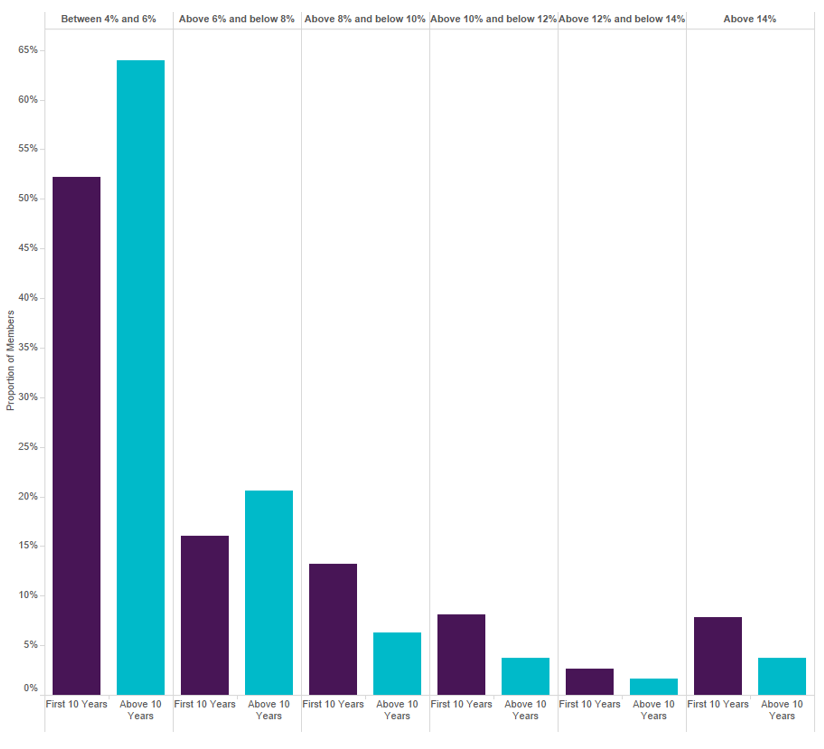

At present, the uncertainty around the future causes many retirees to be conservative in their spending. Graph 1 shows that most retirees draw modest amounts from their pension each year. The majority of those who have been retired for more than ten years still draw no more than 6% of their balance as pension payments. The government hopes this frugality will be overcome by Comprehensive Income Products in Retirement (CIPRs), which are scheduled to be launched from July 2022. However, these products will be voluntary for members and we expect the take-up rate to be low if CIPRs are implemented in the form that is currently proposed.

Graph 1. Distribution of Pension Payments, balances of $100,000 – $1,000,000

Source: Rice Warner’s Super Insights – Percent drawn in first 10 years of retirement against longer durations.

The new Member Outcome tests should eliminate the worst of the under-performing funds. Then, members could focus on the right retirement strategy with less risk of this failing through having the wrong product. If we changed the legislation to allow members to default into a retirement product, the advice they need would be focused entirely on picking the right strategy for their circumstances. It might even be possible to extend intra-fund advice to provide this service in some circumstances. This does assume that the default would be suitable for most members, but that can be assessed as part of the Member Outcome tests.

WHAT ARE FUNDS DOING?

For funds with a large proportion of their membership approaching retirement, waiting for future products to be defined by the CIPR framework would be an increasingly dangerous approach. Among other considerations, criteria for a retirement product suited to their membership will not necessarily be aligned with the CIPR requirements when these are ultimately legislated.

As a result, more funds are prioritising building retirement products and decision-making resources focused on outcomes for their members, rather than waiting for the CIPR legislation. Of necessity, these will be Choice products under current legislation, but may point the way to a much-needed new generation of retirement products that are available on a default basis.

While the industry does not want more change, establishment of default retirement products and a simplified regime for delivering financial advice are critical to improve member outcomes. As new reform takes a while to develop, it is prudent to start that journey now.