Preparing for a market downturn

- On 27/09/2018

- investments, superannuation

The behaviour of stock markets is unpredictable as sentiment plays a big part in short-term price movements. When people are upbeat about the economy, prices often rise exuberantly; when the market turns down significantly, it is usually fast and without notice. So, while we can say that investment markets follow a cyclical pattern, no one can predict when the market will rise or fall. We also know that markets usually recover their losses over time, sometimes quite quickly.

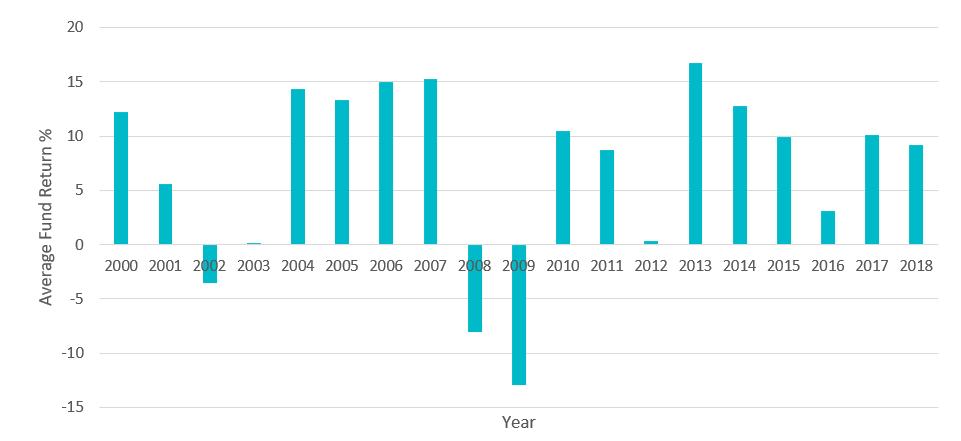

Table 1 shows the aggregate returns of APRA regulated superannuation funds since 2000. Default superannuation fund returns have been positive for each of the last nine financial years, with many close to or above double digits. This current bull run in markets means that a reversal is becoming more and more likely. Could we have a negative 25% return on equities leading to a 10% or more fall in fund returns this year or next year?

Table 1. Superannuation fund returns – 2000 to present

Source: Morningstar data and Rice Warner analysis

If the markets do take a step back, this will have a big impact on superannuation funds and their members, particularly the growing numbers of retirees. The effects could be magnified for members who find that they are bearing more investment risk than they realised and lock in losses by moving to more defensive strategies at an inopportune time. Rather than waiting until the event, funds should prepare now through active communication to those at risk.

Many funds set investment return targets as CPI + 3 to 4% over a rolling ten-year period. Funds should ask themselves whether these targets are realistic (using stochastic modelling) and communicate the risks to members.

The probability of achieving a ten-year return should be lower if you believe there will be a mean reversion in the next ten years. Based on this, should funds tell members that the probability of achieving your target is temporarily lower?

Experience from the previous financial crises shows that many members will switch out of growth assets into cash at the bottom of the market. Recent Rice Warner research showed that the majority of members who have made an investment Choice have selected an option that will likely lead to lower returns¹. Funds should help to educate members on the relevant risks, and segment members into groups to tailor the approach to member needs. For example:

- For members far away from retirement, funds could begin a process of educating them on the risk of a market crash, but more importantly the impact of switching to cash at the bottom of the market. This could help prevent members going into a downturn with more exposure to volatility than they can tolerate.

- For members close to or in retirement who will have upcoming liquidity needs, funds could help members assess their liquidity requirements and encourage members to put away say 18-36 months of expenditure needs (forecast pension payments) into a “cash bucket”. Funds might also encourage members to allocate excess investment returns or income from dividends into this bucket as well to reduce downside risk.

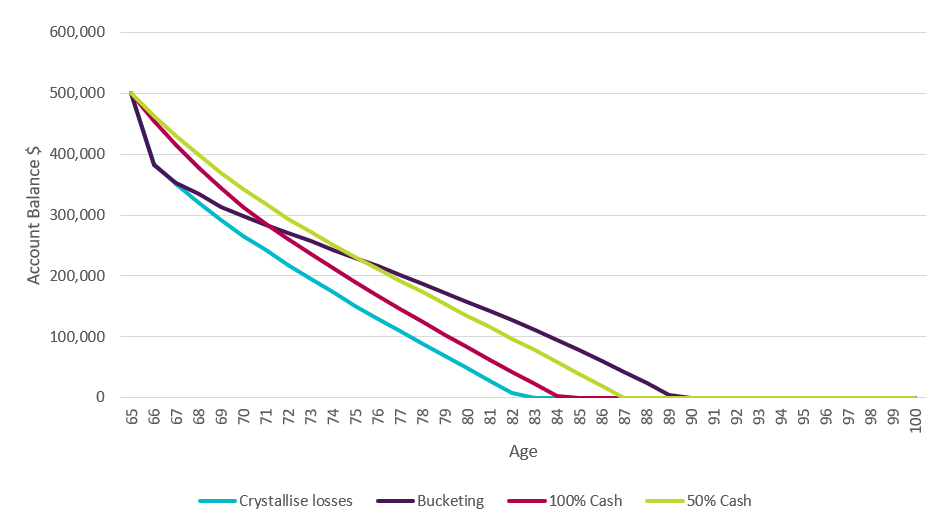

Take for example the following retiring member aged 65 with a $500,000 retirement benefit. They invest an initial balance of $500,000 but immediately experience a market crash. At retirement, the member allocates a year’s cash drawdowns (at the ASFA Comfortable standard) to cash with 50% in a balanced portfolio to cover the following 10 years, and 50% in high growth for the period thereafter.

- The market correction results in a -15% return on high growth and -10% on balanced

- The funds recover back to the base after three years

- The Cash portfolio earns 2.5% p.a., balanced earns 6% and high growth earns 8% p.a. post-recovery

The result shows the simple bucket strategy, sticking to growth will outperform investing higher proportions of the portfolio in cash as well as switching to cash at the bottom of the market.

Graph 1. Impact of investment strategies following market correction

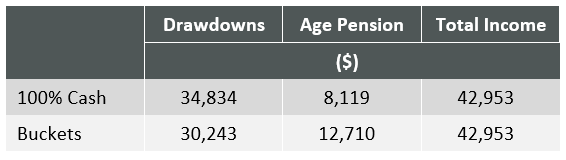

In this scenario, the member benefited from the perversity of means-testing of the Age Pension. As the member’s overall assets fell, the part Age Pension grew. So, the bucketing solution vs. 100% cash meant the member’s Age Pension increased by more than 50% in the first year and drawdowns from superannuation were $4,500 lower.

Table 2. First year retirement income

Effectively, the Age Pension becomes a put option on any downturn in market prices. It also means the member’s Cash bucket lasts longer, allowing a higher chance of recovery without eating into capital.

None of us know when the next stock market correction will take place, but prudent funds should be preparing for a downturn now.

Given asset allocation is the number one driver of net returns to members, taking small and simple steps such as the example above has the potential to protect retirees and deliver a great outcome.

¹ Analysis – MySuper vs. Choice, Rice Warner, 2018, prepared for AIST