How to measure the efficiency of retirement products

- On 19/10/2016

- superannuation

Retirement is the most important aspect of superannuation but measurement of the efficiency of superannuation retirement products is complex and difficult.

It is critical that a satisfactory way is developed to assess the efficiency of retirement products in meeting the varied needs of retirees in the different phases of their retirement. This is a pressing issue given that superannuation fund members are retiring in unprecedented numbers and the vast majority are purchasing retirement products.

Rice Warner expects that the number of retirement members in all super fund sectors to more than double to 4.5 million over the next 15 years and the value of superannuation retirement assets to rise from $631 billion (as at June 2015) to $1.4 trillion (in today’s dollars). And this year alone, some 250,000 new retirees will join the retirement ranks and assets will swell by approximately $35 billion.

Needs test

How efficiently will existing and developing superannuation retirement products meet the needs of retirees throughout their typically long and nuanced retirements? This is a fundamental question facing superannuation funds and the Government*.

It is not easy to answer given the diverse circumstances and needs of retirees. However, all superannuation pensioners have two primary needs:

- Certainty of cash flows and cash to provide pension payments to meet current consumption (living expenses) and contingencies.

- Growth of their capital so future cash flow is sufficient to meet future expenditure needs no matter how long they live.

Neither of these needs or their associated risks can be avoided and both must be managed concurrently. They impose competing investment objectives that cannot be met through a traditional investment strategy.

The requirement for short-term income demands investment in liquid assets that cannot produce sufficient growth.

Yet long-term growth demands investment in growth assets that have inherently volatile market prices. (Consequently, asset values could be depressed when cash is needed.)

Efficiency measures

Superannuation funds should demonstrate how efficiently their retirement products are taking account of the multiple risks facing retirees when attempting to meet the above needs.

These risks include investment risks (not protecting against inflation), longevity risks (outliving savings) and liquidity risks (not having money available for pension payments when due.)

Further, a critical and underlying component in measuring the effectiveness of a retirement products is the net return over the long term, particularly given average life expectancy at retirement exceeds 20 years for most retirees.

Measuring the net return and its relevance is obviously straightforward for account-based pensions, which currently make up the majority of the market.

Retiree circumstances

For most people, a superannuation retirement product is supplemented by the Age Pension, their spouse’s superannuation and by other non-superannuation income. However, the efficiency of a retirement product in meeting their needs still varies significantly depending upon the particular circumstances of individual retirees.

Some retirees will be prepared to accept a lower investment return in order to have greater security of income – a lifetime annuity being the extreme example.

Efficient products

With increased life expectancy, there is a long investment horizon in retirement; requiring growth assets to provide inflation protection and make savings last a long time.

Ideally, this should be done in a way that does not force the sale of assets at depressed values to meet pension payments. The key is to use tools that maximise long-term investment performance while delivering returns in a way that supports short-term income requirements.

We consider that many superannuation funds are too conservative with the portfolios for their account-based pensions. Such funds focus on minimising short-term negative returns but do so by reducing overall investment returns – and the future retirement benefits.

Generally, the optimal solution requires a separation of needs and an allocation of the assets being used to satisfy those needs. This allocation might be nominal or it could involve separation into strategic investment “buckets”.

Assets must be matched to liabilities and this cannot be done with a composite investment approach.

Critically, existing products can be easily tailored to meet these requirements.

An alternative is to use a lifetime annuity to provide all needs in a single product. However, the cost of the guarantee makes these products financially unattractive except at advanced ages.

Example of efficient product

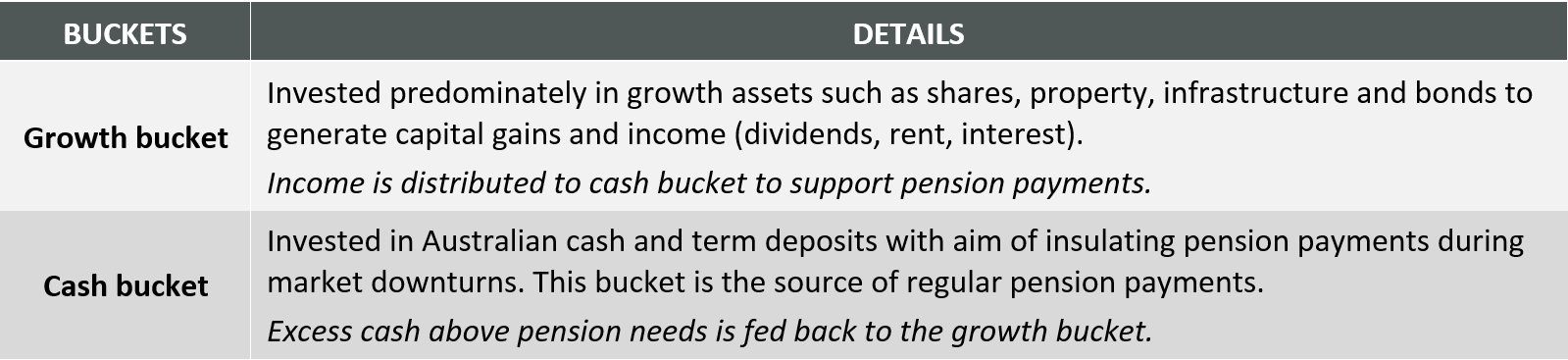

An example of an efficient retirement product is one that takes a long-term investment approach yet uses a bucketing approach – with a growth bucket and a cash bucket to meet pension payments.

The product maximises long-term growth by investing in a growth pool to:

- Harness the equity-risk premium.

- Harness the extra returns from the illiquidity premium from investing in unlisted assets.

- Utilise the valuable franking credits from investments in Australian tax-paying businesses.

This particular product meets a retiree’s short-term income need by operating the growth pool as a distributing trust. This results in all dividends, interest and rents being moved into the member’s cash account. The value of franking credits is also transferred as the dividends are paid (even though the franking credit will only be repaid to the fund after the tax return for the financial year is lodged).

As the running yield on the pension assets will be between 4% and 5%, the cash built up will be very close to the member’s withdrawal requirements.

The key to this solution is that the volatility of capital movements is largely irrelevant to members – they are not being forced to draw their capital down.

Another advantage is that the capital is invested long-term and can access infrastructure and other unlisted assets without worrying about liquidity.

This core strategy can then be enhanced by building a nest egg to meet extra expenditure commitments and contingencies. It is best done by transferring money from the growth pool into cash following periods of strong performance.

Later in life – when lifetime annuities provide better value and making financial decisions becomes more difficult, retirees who want to lock in certainty could convert part or possibly all their accumulated assets to a lifetime annuity. Their assets should have done well from the long-term investment in a diversified growth portfolio and converting into an annuity at any time from age 80 will remove future volatility late in life.

* The Productivity Commission is currently studying how to assess the efficiency and competitiveness of the superannuation system and Treasury is looking at the development of comprehensive income products in retirement (CIPRs).