Financial advice after the super tax changes

- On 08/12/2016

- financial advice

After a long period of opposition, the super changes put up in the May Budget and amended in September have been legislated. It is now over to financial planners to help clients navigate the biggest changes in the super tax system in a decade. While some familiar structures and strategies have been up-ended, the system remains fundamentally attractive and offers many routes for people to achieve their goals (once these have been explained).

The cornerstone of the changes to apply from July 2017 is a maximum of $1.6 million (subject to indexation) that can be transferred into a tax free pension account. Once this cap has been met, or if their combined accumulation and pension account balances exceed it, people cannot make further non-concessional contributions.

Impact on workers

The reduced contribution limits will make it difficult for most workers to reach the pension cap, though it should be noted that under the old rules few people got anywhere near this level of super.

Older workers might have more disposable income but the cap on concessional contributions will prevent them putting a lot away when they are able. The 30% tax on contributions for those with salary/super above $250,000 limits them to a net $17,500 each year. They could also pay up to $100,000 a year of non-concessional contributions until they hit the pension cap but this will be out of reach for most people.

The best way to achieve a high super benefit is to start young and put extra in before age 40. These contributions will multiply through compound interest.

For those who are fortunate enough to need to consider the caps, and have partners, managing super as a couple becomes even more important than before. A wealthy couple could retire with up to $3.2 million in tax-free pension accounts by accumulating their super reasonably evenly. Previously, it did not matter how super was divided between a couple – so long as the relationship stayed together!

Decisions on the optimal mix between super and other financial assets become more complex, and more important. For example, someone retiring with super of $2 million and no mortgage could previously have kept it all in a tax-free account-based pension account. Following the changes, the account based pension is still the natural home for $1.6 million, but where should the other $400,000 be invested? A super accumulation account would involve tax of up to 15% – which could compare favourably with holding the assets directly if returns are taxed at 49%.

However, someone without other taxable income holding the $400,000 directly will pay little or no tax on their investment earnings outside super. So, they may prefer to move the money out of the accumulation account.

The increased use of investments outside super will encourage more people to make financial decisions on a whole-of-wealth basis.

The changing environment gives financial planners the challenge – and opportunity – to help their clients to:

- Manage savings as a family – couples co-ordinating their plans have improved chances of being able to make catch-up contributions tax effectively after a career break to look after young children.

- Deal with greater complexity – the super tax changes have not only increased the complexity of super, but has also increased the range of structures and strategies that should be considered.

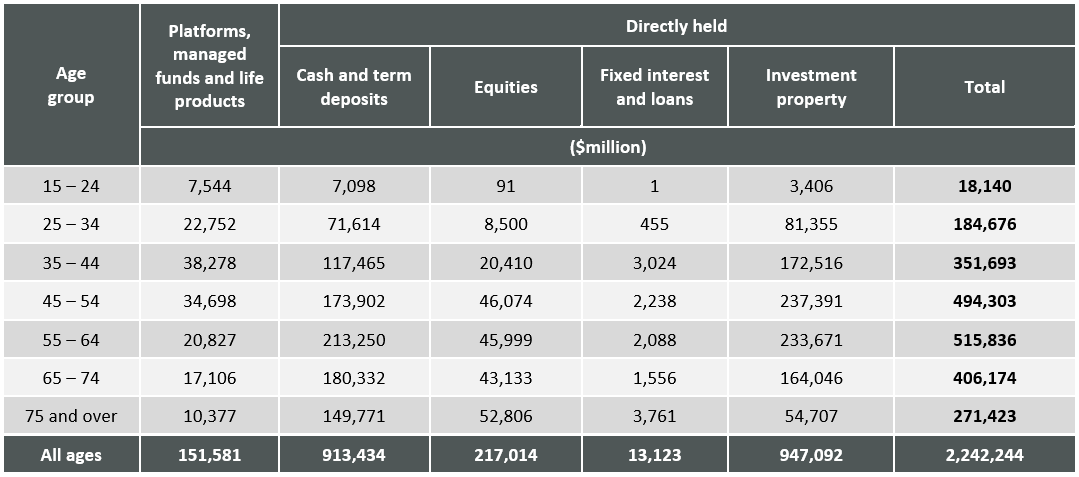

- Make decisions on a whole-of-wealth basis, not just in product silos. When considered as a whole, investments held by Australian households outside super have comparable financial significance to the super system. The table below shows their importance both in accumulating wealth, and in using it to finance retirement income.

Total personal investment holdings by age at 30 June 2015

Source: Rice Warner Personal Investments Market Projections 2015