Does robo advice compute?

- On 07/07/2016

The increasing attention in Australia to technology-driven financial advice, dubbed robo-advice, raises numerous questions for investors, super funds, fund managers and financial advisers.

What is robo-advice?

Robo-advice, commonly referred to as digital advice and automated advice, is built on a foundation of rules and algorithms using client data to drive automated advice recommendations.

In broad terms, a calculation engine or platform will power a robo-advice tool. These engines and platforms house the rules and algorithms which consider variables such as scenario (singles/couples), age, gender, assets (superannuation and personal investments), income, debt, financial objectives and tolerance to investment risk. Risk has traditionally been described in terms of a person’s aversion to capital losses (that is, market volatility). More recently, it has moved towards the probability of achieving a targeted objective, such as the level of income in retirement.

The actuarial sign-off of these engines and platforms is an important component of the comfort and security that users will seek when relying on recommendations from advice technology. In particular, providers of advice technology solutions will want to ensure, and certify, that their advice solutions are accurate and compliant.

It is relatively early days for advice technology, with solutions only scratching the surface on a range of advice topics and strategies, including adequacy of retirement income, adequacy of insurance, transition to retirement, contributions optimisation, debt, investment and client profiling. Advice needs to be provided for couples and this requires data often not held.

The advice tools can support a self-directed or guided experience and can be delivered across multiple channels including a desktop computer, tablet or smartphone. Currently, advice being provided by robo-tools is relatively basic but will become more sophisticated as the environment matures.

Ideally, robo-advice technology will reduce the cost of advice, make advice more accessible, and improve the consistency of advice. Ultimately, these developments will assist in the education of members, resulting in enhanced levels of financial literacy and member engagement.

How is robo-advice likely to evolve in Australia?

Based on overseas experience, it seems that “personal” robo-advice (as distinct from “general” advice) will generally fall into one of the following categories:

- Fully-automated advice with no human inter-action.

- Hybrid services that start with fully-automated advice, with various levels of sophistication, supplemented with the option of consulting a “human” adviser.

- Full-service traditional advisory services that leverage guided advice technology solutions. This model is a logical development of existing full-advice services typically aimed at wealthier clients with more complex issues.

Technology developments allow the delivery of scalable on-line advice tools to a large audience in a cost efficient manner. Properly utilised, robo-advice will allow providers of advice to extend their value proposition to target those investors who historically have not had sufficient assets to meet the current business models. This will likely include many younger investors.

Further, the arrival of robo-advice may enable traditional advisers to concentrate more on their roles as behavioural coaches, urging investors to adhere to their long-term objectives and not to allow emotion to dictate investment decisions.

What are large super funds likely to do with robo-advice?

Super funds are likely to rely more on advice technology as a means to improve and expand their existing advisory services, member engagement and business intelligence.

Super funds are likely to seek further development of the self-directed and guided advice tools already provided by Rice Warner. These include calculators covering adequacy of retirement savings, contribution optimisation, insurance needs and risk profiling. The calculators are designed to let members know their current position and how to improve that situation; effectively providing a call to action.

The role of robo-advice, in combination with advisory services, needs to be well thought through. What function the technology plays, whether that is self-directed or guided, will depend on what role the funds want their financial planners to play in the value chain. It will benefit funds by increasing engagement levels and in turn, will ensure insight into member’s behaviours is captured via data analytics.

Is robo-advice the silver bullet?

Quality low-cost robo-advice could be something of a panacea for the vast majority of investors/savers (perhaps 80% of adult Australians) who have never consulted a financial planner or can’t afford to.

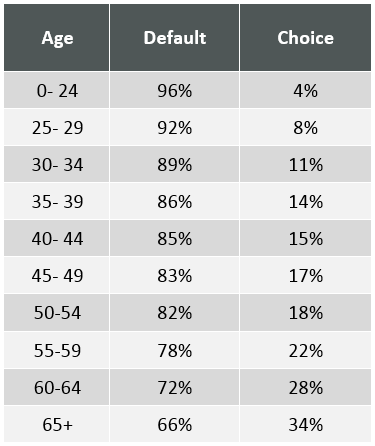

The table shows the proportion of super fund members that effect investment choice within their superannuation fund. Overwhelmingly, the vast majority of superannuants do not make an investment choice and rely on the default. However, Choice grows with age and account balance.

Source: Rice Warner, Super Insights 2016

Robo-advice provided on a large scale could help address Australia’s persistent low level of financial literacy that remains despite repeated messages about the inadequacy of retirement savings.

What about more complex issues?

In the short to medium term, it is not likely that robo-advice will reach the point of being able to completely satisfy the needs of clients with particularly complex issues unaided. Such clients may have family trusts, small-medium businesses, complicated tax affairs and estate planning concerns. The tools are generally capable of dealing with these issues, but they need to be guided by someone with experience especially when there could be complex interactions between the advice topics.

Do super funds know enough about their members to provide personal robo advice?

Many industry funds, do not know their members’ incomes, total super and non-super assets, marital status, partner’s assets and superannuation, liabilities or financial goals. Members needing advice on even the simple topics need to provide this information. The introduction of robo advice will provide an opportunity for super funds to get to know and segment their members much better.

Must robo-advisers be licensed?

ASIC emphasises that the required “standards that apply to robo-advice and advice delivered by a human are identical”. A provider of robo-advice needs to hold an Australian Financial Services Licence (AFSL) or be a representative of an AFSL licensee.

Many of the proposed robo-advice providers in Australia intend to offer scaled or limited personal advice rather than comprehensive advice, according to ASIC.

The advice must take personal circumstances into account. “Any robo-advice model that results in all consumers receiving similar advice will raise a very serious red flag for us,” ASIC adds.

Yet no matter the future of specialist robo advisers, it is inevitable that the use of financial technology in the provision of all types of financial advice is inexorably set to grow.

1 Comment