Productivity Commission – Four different groups of superannuants

- On 28/09/2016

- commission, retirement

The Productivity Commission’s investigation into competitiveness and efficiency in the superannuation industry intends to take a ‘whole of market’ view when assessing the industry on a number of efficiency measures. However, we note that although this view of the market may be useful the market itself is not homogenous. It is important to consider the make-up and requirements for different segments of the market when interpreting the performance of the industry. This is especially important when assessing how the market meets different member needs as well as correctly attributing decisions to those who made them.

The recent Rice Warner submission to the Productivity Commission identified four major segments in the Superannuation market;

- MySuper

- Choice

- SMSFs

- Retirement

The most significant variations in the market are attributable to the divide between these segments and each of these groups show large differences in distribution of account balances, age, engagement and needs. More importantly, each of these groups has its own objectives.

Default Members

Default members are those who are in the default MySuper product. This is the largest group of superannuants in terms of membership. They tend to have low balances, are younger and are more likely to be female. This group also makes up the majority of inactive accounts. The median balance for default members is under $10,000.

We consider that the main focus of default members will be on maximising their balances prior to retirement. Since they are less likely to make additional contributions their balances are susceptible to erosion through fees and insurance premiums. Low levels of engagement generally mean that member services and financial advice are under-utilised by this group and add little value (at least at this stage of their working life).

Choice Members

Choice members are those members who have remained in APRA regulated Superannuation Funds but have chosen their own investment strategy. These members tend to be older, with higher balances and are also more likely to be male. We have observed that there is a strong correlation between age and the percentage of members who have made investment choices. However, default members still make up the majority of accumulation accounts at all ages.

Choice members have materially higher account balances. They are also more highly engaged with their superannuation and are much more likely to utilise additional services and receive advice. We have observed that they also opt into increased insurance cover. Similarly, to MySuper members, net returns and competitive fee structures are also needed to help achieve their balance at retirement objectives.

SMSF Members

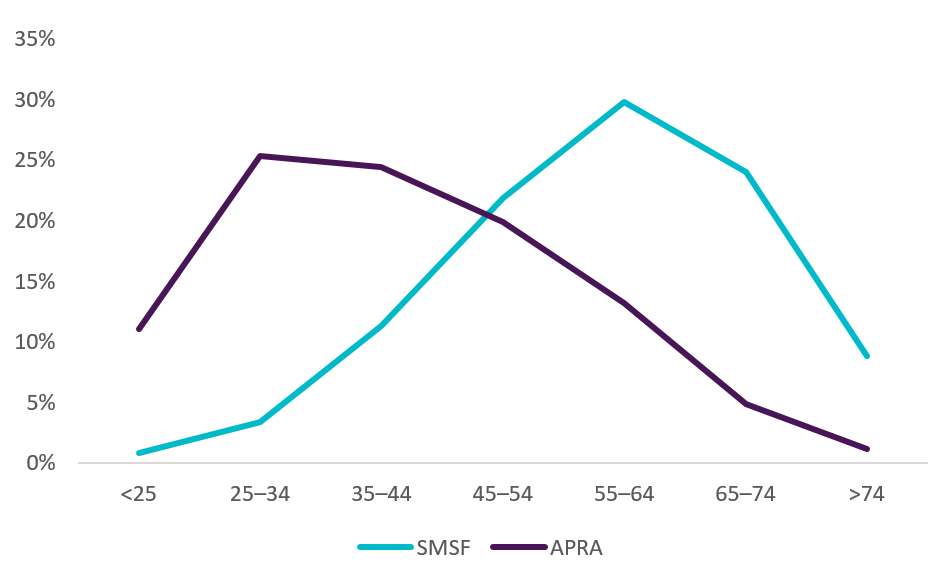

SMSFs have taken the responsibility for managing their superannuation into their own hands; some SMSF members do this under the advice of financial planners or accountants. These members have the highest average balance of any segment and represent close to 30% of all superannuation assets. They are also much more likely to be retired (or transitioning to retirement) with over half the SMSF assets in the retirement stage.

Age profile of SMSF members and APRA fund members

ATO SMSF Statistics July 2015 & APRA Fund Level Statistics 2015

Running an SMSF comes with high fixed costs, and they usually rely on scale in order to be competitive with APRA funds. Ultimately there is a requirement for SMSFs to keep costs at a reasonable level to avoid unnecessary erosion. Rice Warner previously provided research to ASIC on this issue which concluded minimum balances of $200,000 to $500,000 were required depending on the level of administration the trustees were willing to undertake. ¹

SMSF’s also allow for access to investment assets that are not traditionally offered through funds, specifically the availability of unlisted assets and the ability to gear property investments. A further area which the Productivity Commission has recognised is the management of tax. SMSFs manage tax at the individual member level which provides additional flexibility. For example, members move into retirement without triggering a tax event. Therefore, the deferred tax liabilities held on the accumulation accounts are voided on moving into pension phase.

Retirees

Retirees are highly diverse in terms of accounts balances making up roughly one third of all industry assets. Unlike the other segments, there are no specific demographic indicators for this group (apart from the fact that they are wealthier than those who have little superannuation). Retirees also have very different needs compared to accumulation members, primarily due to the fact that they are drawing down on benefits rather than focusing on accumulating as large a benefit as possible.

Pensioners have two primary needs:

- Certainty of cash flows and cash values to meet current consumption (living expenses) and contingencies.

- Growth of their capital so future cash flow is sufficient to meet future expenditure needs no matter how long they live.

These two needs create a difficult balancing act which is difficult to manage through traditional investment strategies. The short term demands of the retiree for pension payments requires a holding in liquid assets, yet most of the benefit needs to be placed in volatile growth assets.

¹ Costs of Operating SMSFs, Rice Warner, May 2013 http://download.asic.gov.au/media/1336058/cp216-RiceWarner-cost-of-operating-smsfs.pdf