Understanding member behaviour

- On 05/10/2016

- mySuper, superannuation

There is currently no means to measure the quality of decisions by superannuation fund members. This is despite most members being able to choose their superannuation fund and their investment strategies.

As Rice Warner states in its recent submission to the Productivity Commission’s draft report, How to Assess the Competitiveness and Efficiency of the Superannuation System, we need to understand the choices members make and whether those choices are rational.

Psychology of financial decisions

We suggest there is a need for a greater involvement of behavioural finance, the psychology of financial decisions, to observe decisions of members in order to minimise those likely to lead to poor outcomes.

This leads to a fundamental question: What choices should be provided in a compulsory system with significant tax-concessions?

Certainly, a material proportion of members do not make a fund or investment choice – just under 90% of members aged under 24 to 47% for members approaching retirement. These comprise members who do not exercise available choice (the vast majority) and many who do not have the ability to make choices because of their employment arrangements.

It is logical that any analysis of member behaviour concentrates mainly on those who exercise fund and/or investment choice.

Choice members are classified as those who have remained in an APRA-regulated fund yet have made a fund choice OR an investment choice, in contrast to default members who are in the default MySuper product chosen by their employers.

Nevertheless, it should be recognised that members who do not currently make a choice and are in default funds may choose to exercise choice in the future. An extreme example could include making an emotionally-driven decision to switch from a balanced MySuper default fund to an all-cash portfolio in response to, say, a short-term downturn in equity prices.

SMSF members have, of course, exercised choice by choosing to take responsibility for managing their superannuation. Again, understanding the behaviour and decision-making of SMSF members is critical.

‘It’s my money’ – but not yet

A prevailing view appears to be that fund members can do what they like in terms of the investment of own superannuation savings within the broad rules; after all, “it’s my money”. However, the growth in choice members and in SMSFs together with the continuing tax concessions suggest that the quality of their financial decisions should be monitored.

Behavioural economists tell us it is incorrect to make an underlying assumption that individuals will make rational decisions in regard to their financial well-being.

We would expect that logical decision-making would lead to a focus on the maximisation of retirement outcomes. Logically-thinking fund members would presumably attempt to maximise their long-term returns in accordance to their risk profile and to minimise investment costs where possible.

However, behavioural economists have identified a series of common behavioural traits or biases among investors that can be detrimental to their financial well-being.

These include:

- Overconfidence in their investment abilities.

- Being overly-sensitive to short-term market movements.

- A tendency to following the investment herd, seeking perceived safety in numbers.

- this leads to buying at market highs and selling at market lows due to recent investment performance.

Another common behavioural trait among investors is simply inertia. This includes postponing decisions to set an appropriate strategic asset allocation and/or to adequately save for retirement.

Some behavioural economists have tagged excessive choice as the phenomenon of “choice overload”, warning that it can lead to reduced investor participation and to investors gravitating to the most familiar investment options such as term deposits.

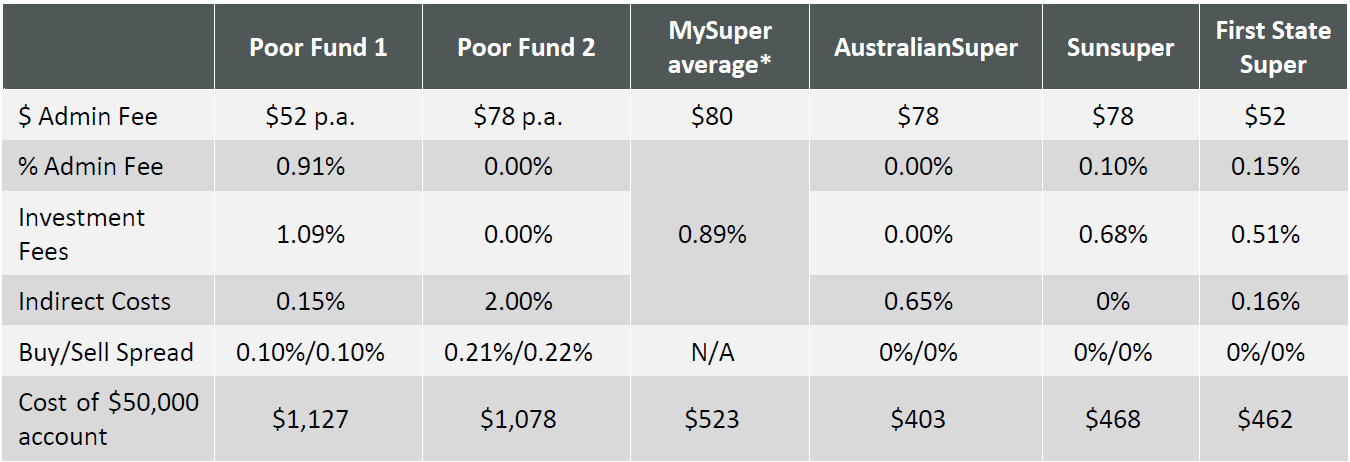

Selling emotion, not value

By their nature, individuals are vulnerable to letting emotions dictate their investment decisions, again as behavioural economists emphasise. An almost textbook example of superannuation funds that could be considered inappropriate are a few of the high-cost “social impact” products.

These particular funds are selling an emotional proposition without alerting would-be members to the high costs, which are extremely high compared to the general MySuper market, and the impact of those costs on their likely investment outcome.

We question the extent to which a member is acting rationally and in their own best interests by opting to move to a higher-cost provider of a “Socially Responsible Investment” (SRI) when much-lower cost SRI alternatives exist (table below).

Comparison of SRI fees

* Analysis of APRA Quarterly MySuper Statistics June 2016

Researching member behaviour

In broad terms, Rice Warner’s research shows that members are more interested in exercising fund and investment choice as they grow older and their balances increase. Compared to default members, choice members have a higher exposure to cash (much higher), fixed interest and Australian equities and a lower exposure to international equities and alternatives.

The greater exercising of choice by older, bigger-balance members, as shown in our research, increases their vulnerability to making investment decisions against their own interests.

What should be done

It is in the superannuation funds’ interests to better understand the decision-making of their members. This will assist the funds to provide more appropriate, appealing and meaningful education and products.

Such education should, of course, effectively emphasise the benefits of avoiding short-termism, focusing on the long-term, setting and adhering to an appropriate strategic or target asset allocation, minimising investment costs, understanding compounding and taking quality advice where appropriate.

Large funds that understand more about their member behaviour are better-placed to stem the flow to SMSFs, particularly among older members, and to high-cost funds selling emotion.

Good superannuation funds respond to the reality that prospective members may not read product disclosure statements or fee explanations by demonstrating their value to members through their marketing and websites. This is typically not the case with costly poor funds with a sales pitch based on emotion, not on what is in the best financial interests of members.

By better understanding and broadly segmenting their members in terms of differing needs, differing tolerances to risk and differing behavioural traits should enable the choice regime to work more effectively in the best interests of the members and the funds.