Super at a Crossroad

- On 22/12/2020

- projections, research

While the superannuation industry is used to annual changes, 2020 has been a year of turmoil. The year commenced with uncertainty following the onset of COVID-19, followed by the Early Release Scheme (ERS) as part of the plan to support the economy during the lockdown.

Beyond the virus, the year saw unparalleled legislative change, including:

- Introduction and implementation of the ERS.

- Implementation of Putting Members’ Interests First.

- Introduction of the Your Future, Your Super budget measures.

- Release of the Report of the Retirement Income Review.

- Implementation of the Member Outcomes SPS515 legislation.

- Release of the second annual APRA Heatmap.

- Introduction of further Royal Commission recommendations into Parliament.

Impact of new legislation

Over the next 15 years, the superannuation industry will evolve to be a more mature and sophisticated industry. In this year’s Rice Warner Superannuation Market Projections report, we predict that:

- Most superannuation funds will outsource basic administration functions such as transactions processing, unit pricing and member statements as these are commodity services with low fees based on volumes. However, most other services will be self-administered.

- Funds will set up retirement solutions as a different business with specialised administration (not yet available), financial advice and product structures that are tailored to members.

- Superannuation funds will be required to hold more capital.

- Future consolidation will lead to a dozen very large funds, most with some degree of in-house investment capability.

- The funds will invest more outside Australia. Within Australia, there will be high levels of unlisted assets (direct company ownership, property and infrastructure) and proportionally less listed assets – due to the size of the Australian savings pool relative to the market capitalisation of the tradeable markets.

- The retail segment will be transformed. Legacy products will be converted to MySuper and it is likely that there will be ownership changes. The major life companies operating in Australia are now all foreign owned. Will retail superannuation be similar?

- The retail life insurance industry is struggling with unprofitable products and a changing model for remunerating advisers. Conversely, life insurance through superannuation is already more than 60% of all insurance in Australia and, even with the removal of mandatory cover for young Australians and those with small accounts, it should become an even larger proportion of the total life insurance market in future years.

- The financial advice regime is in a period of transition. The legislation is prescriptive and has not kept up with changes in technology that provide the opportunity to deliver advice efficiently on a mass-customised Funds need to work out how to deliver comprehensive advice profitably and at a reasonable price to members.

- Funds will target families rather than individual members and provide support for couples in the same way SMSFs do today. This will deliver tailored and more appropriate outcomes to members.

- Funds could leverage their strong investment capacity to provide access to investments (outside superannuation) for medium term savings such as providing for school fees or home deposits.

Change in segments

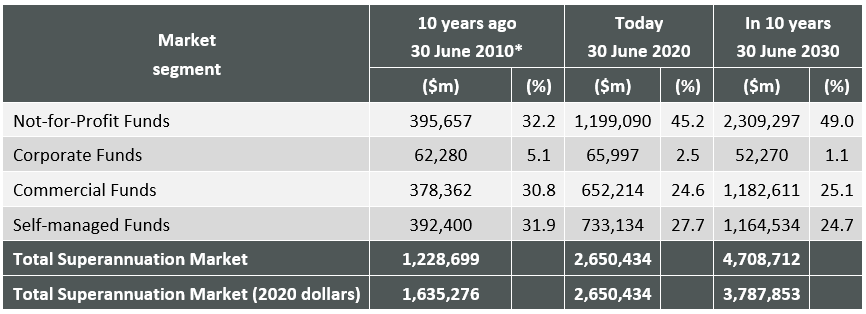

The industry funds together with public sector funds have grown market share annually for 30 years. The trend has accelerated in the last decade and will continue until they become half the market. Corporate funds have been on a downward trajectory since the start of the Superannuation Guarantee in 1992 and the recent Budget’s stapling concept will lead to fewer corporate funds in time. We expect that the retail sector will stabilise at about a quarter of the market and will be much more competitive as they finish removing legacy products and processes.

The SMSF segment grew by consolidating family accounts and making good use of tax concessions. Its market share has been declining as large older funds begin to close. It should also stabilise at about a quarter of the market – or less if APRA-regulated funds sort out their administration.

Table 1. Superannuation assets 2010, 2020, 2030 (nominal dollars)

* This figure is based on historical Consumer Price Inflation (CPI), not the 2.2% CPI inflation rate assumed for projections.

Note that this table does not include $213 billion of employer receivable liabilities, or any lost assets currently held by the ATO.

Projected Results

Over the next 15 years, the market will grow at a lower rate than the last two decades. Lower fund earnings and slower population growth will lead to a compound annual growth rate (CAGR) of about 3.6% a year.

Retirement assets will grow by about 5.4% a year for the industry/public sector segment and about 4.8% a year for the commercial funds. Yet, there will be a slow-down in the growth of SMSFs as more of those large funds wind-up as their members die. This segment will grow by only 1.5% a year which holds the total retirement growth to 3.4% – a little less than the growth of accumulation funds.

Implications

Our projections indicate that market dynamics will shift in the next decade. To remain competitive funds will need to ensure that they can deliver quality outcomes to members both in current conditions and in the context of ongoing market development and change.